In Wisconsin, there are a range of different trust structures available to best suit your specific estate planning needs and circumstances. Common types of trusts include revocable trusts and irrevocable trusts, but there are a variety of options to explore to serve your unique purpose. Given the complex rules and regulations accompanying trusts, it is important to consult with an experienced trust attorney in Wisconsin to find the best trust for your specific needs.

Trusts are powerful estate planning tools that allow one party (the trustee) to hold properties or assets for the benefit of another party (the beneficiary). Trusts are created by a grantor/settlor who transfers some or all of their assets into the trust for the trustee to be responsible for.

Revocable Trusts | Irrevocable Trusts | Special Needs Trusts | Irrevocable Life Insurance Trusts | Charitable Remainder Trusts | Charitable Lead Trusts | Testamentary Trusts | Spendthrift Trusts

To receive means-tested public benefits such as Medicaid and Supplemental Security Income (SSI), people with disabilities cannot exceed an Asset Limit, which is the amount of available assets in excess of the applicable amount. However, assets held in a Special Needs Trust with the disabled individual as the beneficiary do not count toward their Asset Limit. The assets in the trust cannot be paid directly to the beneficiary and must only be used for things the beneficiary cannot obtain through public benefits; otherwise, the disabled individual’s public benefits will be discontinued.

An irrevocable life insurance trust allows the grantor to remove taxable assets from their estate and transfer them to a separate legal entity (the trust) and are powerful wealth transfer mechanisms. The trust is a legal arrangement where a trust owns a life insurance policy, rather than the insured person themself. At the time of the insured person’s death, the life insurance policy proceeds are paid to the trust and then distributed to beneficiaries as the trust outlines.

The trust is irrevocable, meaning that the grantor forfeits all rights to the property contained in the trust, which allows the assets to potentially avoid estate taxation as they are not considered one’s property. An irrevocable life insurance trust also helps with asset protection as creditors should not be able to attack the assets because they belong to the trust, not you. It can also help with funeral or other estate expenses by providing liquid assets that aren’t tied up in a business, real estate, or retirement accounts.

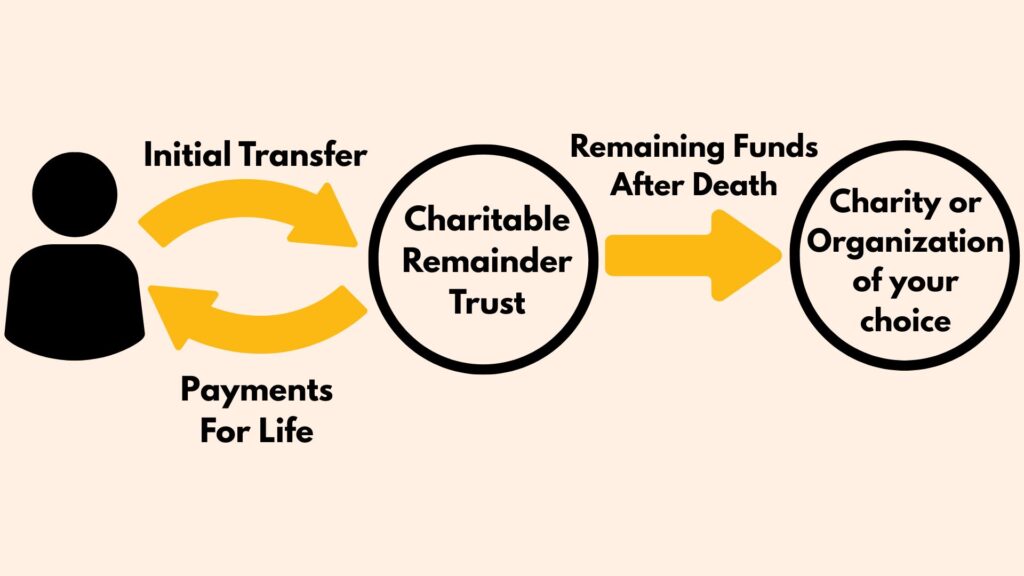

Charitable Remainder Trusts allow you or other named beneficiaries to receive a certain predetermined amount in the form of reliable payments from the trust for life or up to 20 years. Then, the remaining balance of the trust goes to a charity organization of your choosing. The Charitable remainder trust is best suited for beneficiaries who depend upon the money from the trust as their main source of income. On the other hand, a Charitable Lead Trust outlines a certain amount of its income to a charitable organization and the remains will be disbursed to the beneficiaries, putting the focus on the charity rather than its beneficiaries unlike the Charitable Remainder Trust.

Charitable Remainder Trusts are irrevocable, meaning that it is extremely difficult to amend or terminate early once it has been established. The Charitable Remainder trust also offers some benefits, such as tax benefits available immediately to the donors of the trust after its creation and other benefits when it comes to reducing estate taxes.

There are two types of Charitable Remainder Trusts: annuity trusts and unitrusts. An annuity trust pays you the same dollar amount each year that you choose at the start and payments remain the same regardless of fluctuations in trust investments. The unitrust, on the other hand, pays you a variable amount based on a fixed percentage of the fair market value of the trust assets. So, if the value of the trust increases, your payments increase; but, if the value decreases, your payments decrease.

A charitable lead trust is designed to provide a stream of income to one or more charities for a specified term, with the remainder transferred to non-charitable beneficiaries. It is the opposite of a Charitable Remainder Trust, which provides income to beneficiaries and the remainder to charity. A Charitable Lead Trust reduces a beneficiary’s potential tax liability by decreasing the amount they would inherit.

Upon its distribution of funds, a Charitable Lead Trust can be reversionary or non-reversionary. A reversionary Charitable Lead Trust means that the balance of the trust is paid out to the original donor of the funds. A non-reversionary Charitable Lead Trust means that it is disbursed to different beneficiaries than the original grantor.

The initial one-time donation to set up the trust is tax-deductible. However, the trust is not tax-exempt and any investment earnings that the trust accrues are taxed to the grantor of the trust.

Similar to Charitable Remainder trusts, Charitable Lead Trusts are irrevocable, meaning that it is extremely difficult to amend or terminate early once it has been established. This also means that it is usually not possible to change the charitable beneficiary of the trust, the non-charitable beneficiaries, or the term or amount of payments.

Additionally, there are two payout structures with a Charitable Lead Trust: annuity and unitrust. An annuity payout is a fixed amount that must be paid out to charity annually. The annuity amount is determined by a stated percentage of the initial value of the trust so investment performance or changes in the amount in the trust is not taken into account. On the other hand, a unitrust payout is may change year to year as it is determined using the same percentage of the reevaluated value each year, meaning that investment performance is taken into account.

Spendthrift trusts limit a beneficiary’s access to the assets in the trust and can help protect them from creditors. A spendthrift trust is best suited for beneficiaries that you may have concerns about being “bad with money” or unable to responsibly manage their wealth. Creditors cannot access trust funds or assets and beneficiaries cannot take loans out against the trust funds.

The beneficiary of a spendthrift trust is never the trustee, meaning they are not responsible for the assets in the trust. The trustee can spend the money for the beneficiary’s needs to make payments directly to the beneficiary depending on what the trust document allows. Spendthrift trusts are structured to prevent the beneficiary to be wasteful of their trust fund and some are even set up to grant the trustee the power to cut off benefits of a beneficiary who becomes self-destructive, such as with their use of drugs or alcohol.

It is essential to hire an experienced Wisconsin Trust attorney to help navigate the complex legal and tax issues that come with trusts to best ensure that your family and assets are protected. Contact Konstantakis Law Office today to learn what trusts are best for your estate planning needs.